By Conor Larkin, Associate Vice President – Harnham

By Conor Larkin, Associate Vice President – Harnham

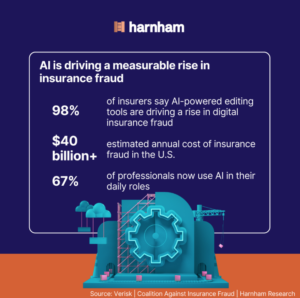

Insurance fraud costs the U.S. industry over $40 billion each year.

What used to be manual and easier to trace is becoming faster, more scalable, and harder to verify. The use of AI tools to generate and manipulate evidence is a big part of that change.

At the same time, insurers are under pressure to improve detection rates, reduce losses, and maintain customer experience. AI is now central to how that gets done.

AI-driven fraud detection is the use of machine learning models to identify suspicious claims patterns at scale.

For insurers operating in high-exposure regions like New York, New Jersey, and Connecticut, this is already changing how fraud teams are structured and how claims are assessed.

Why fraud is becoming harder to detect

AI is now being used on both sides of the problem.

Tools that can edit images, generate synthetic content, or alter documentation are making it easier to submit convincing fraudulent claims. Verisk’s research points to a rise in fraud linked to AI-powered editing tools, particularly in claims involving visual evidence.

Traditional fraud detection systems were not designed for this. Rules-based models rely on known patterns. They struggle when those patterns change.

With fraud becoming faster, more sophisticated, and harder to detect using static rules alone, detection needs to move at the same pace.

Why fraud risk is higher in tri-state markets

In markets like New York, where claim volumes and policy density are high, insurers are already applying AI to reduce false claims and improve detection accuracy.

- High claim volumes

- Dense and varied customer populations

- Strong regulatory oversight

- Greater exposure to organised fraud

This combination is forcing faster adoption of AI-driven fraud detection.

Where AI is improving fraud detection outcomes

AI is not replacing fraud teams, but it is changing how claims are assessed, prioritised, and processed.

The impact is concentrated in three areas:

Claims triage and prioritisation

Models score claims based on risk, using claims history, behavioural patterns, and supporting data. High-risk cases are flagged earlier, allowing investigators to focus where it matters.

Pattern and anomaly detection

Machine learning identifies connections across large datasets, including relationships between claimants, unusual behaviours, and emerging fraud patterns that are difficult to detect manually.

Reducing manual review

Low-risk claims can move through faster, supported by automated checks across structured and unstructured data, including documents and images.

AI models are effective because they can assess risk continuously across multiple data sources, rather than relying on fixed rules at a single point in the process.

What limits AI fraud detection: data, governance, and talent

AI is not the primary constraint in fraud detection. Execution is.

Insurers need to manage model accuracy and bias, data quality and availability, regulatory compliance, and explainability of decisions. All of these challenges come back to data.

Harnham’s research shows that as companies scale their AI investment, the focus is shifting toward the critical “unseen” infrastructure: data engineering and governance. In a regulated environment, models are only as valuable as they are traceable. Without reliable pipelines and defensible logic, progress stalls at the pilot stage.

You need:

- Machine Learning Engineers to move models from labs to production.

- Data Engineers to secure the underlying foundations.

- Governance Specialists to ensure compliance is “baked in,” not an afterthought.

- Analytics Leaders to translate model outputs into commercial decisions.

While 67% of professionals now use AI in their daily roles, the market remains short on talent that can bridge the gap between technical capability and commercial execution.

What to focus on when scaling fraud detection with AI

For tri-state insurers, the priority is applying AI to improve how fraud is detected and managed. That means moving away from isolated tools and embedding AI into how claims decisions are made.

This takes:

- Clear ownership: Fraud detection strategy is tied to specific claims outcomes, with defined accountability.

- Data foundations: Pipelines support consistent, reliable model performance.

- Targeted hiring: Teams combine technical capability with an understanding of how fraud impacts cost and risk.

Execution is where results are won or lost.

Harnham supports insurers in building the teams required to deliver this, from defining roles aligned to fraud detection outcomes to providing access to specialist AI and data talent.

The focus is on making AI usable within existing operations, not adding complexity.

AI is now part of how fraud is created and how it is detected.

For insurers in high-exposure markets, the priority is clear: build the data foundations, deploy the right models, and put the right teams in place to make them work.

If you’re reviewing your fraud detection strategy or planning your next AI hire, speak to Harnham.